The Hidden Cost of Government Payments: Design, Behaviour, and Friction

- Richard Laycock

- Jun 1

- 3 min read

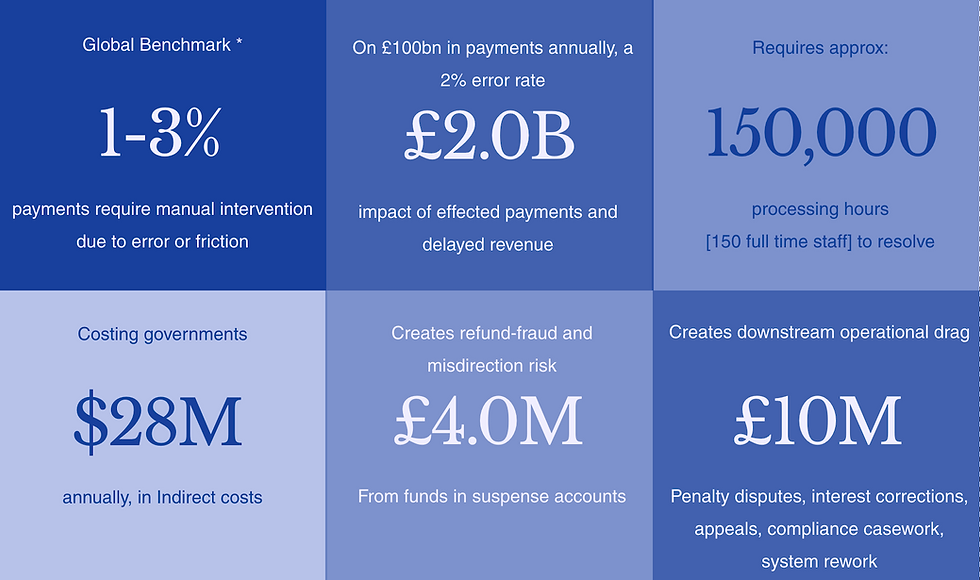

Efficiency isn’t lost in operations — it’s often lost much earlier, at the moment government designs payment systems that don’t match how citizens actually live, pay, and behave. When you connect these behavioural and design-driven frictions with global benchmarks, the scale of the hidden cost becomes harder to ignore. The World Bank’s Global Payment Systems Survey suggests that manual intervention and exception handling remain persistent features of national payment systems, typically affecting around 1–3% of transactions across both advanced and emerging economies. IMF operational cost methodologies reinforce the same point: even small levels of friction can scale into disproportionately large fiscal and service burdens at government volume. These are not marginal issues; they are system-level.

Citizens behave according to trust, familiarity, and control. People who use cards for most everyday purchases will naturally expect to use the same (or a similar) method when paying government. When the system instead nudges them toward a non‑familiar route—often because those channels appear cheaper on paper—the outcome is predictable: higher error rates, more failed payments, more inbound calls, more manual reconciliation, and more operational rework. In practice, the friction rarely disappears; it shifts. And it usually lands on the system (and sometimes on the citizen, through late-payment penalties).

The same is true when design choices create avoidable opportunities for human error. Allowing free‑format reference entry on bank transfers—with no validation or guardrails—predictably increases mis‑keyed references, misapplied payments, suspense items, and rework. These are not just operational issues; they are design and control issues. And they are foreseeable, because they reflect how people behave when making payments in the real world.

These frictions are often compounded by the way government is organised. Payment design may not have a single end‑to‑end accountable owner; instead, responsibilities are commonly fragmented across Finance, Operations, Treasury, Digital, Commercial, and policy teams—each optimising for its own priorities, constraints, and incentives. Finance focuses on reconciliation. Operations focuses on throughput. Digital focuses on channel adoption. Treasury focuses on liquidity. Commercial focuses on vendor cost. Policy focuses on delivery speed. What can get lost is ownership of the end‑to‑end citizen experience and the total system cost. The result is a payment landscape shaped by compromise rather than coherence, where behavioural insight is not consistently embedded and operational consequences are absorbed downstream.

Global benchmarks make the scale of this friction easier to see. As an illustrative example: for a department receiving $100 billion in payments annually, a 2% friction rate (within global norms cited in the World Bank survey) affects $2 billion worth of transactions. Resolving those exceptions can consume around 150,000 hours of processing effort (roughly 150 full‑time staff), and may generate indirect costs in the tens of millions per year using IMF‑aligned exception‑handling economics. Add losses from refund fraud and misdirection risk from suspense accounts, plus downstream operational drag from disputes, corrections, appeals, and compliance casework, and the scale of the hidden cost becomes clearer.

Every payment that fails, stalls, or misfires costs governments far more than the value of the error itself—because even a 1–3% rate of human error and payment friction can translate into tens or hundreds of millions in avoidable operational costs at scale. When you also consider the impact of delayed revenue recognition—money that should be available for critical services like education, healthcare, policing, and defence—the pressure on the public purse can increase further.

Much of this is not fundamentally caused by inefficient operations. It is driven by design choices that don’t fully account for real-world behaviour—and by governance structures that make it difficult for any one leader to see (and manage) the system end to end. Fragmentation means each directorate may only experience a slice of the friction, so the whole picture is easy to miss. The result is persistent inefficiency that can rival, and sometimes exceed, more visible loss types—because it is structural and repeats daily.

The opportunity is that citizen behaviour is one of the more predictable elements of the system. People use what they already use. They trust what they already trust. They avoid what feels unfamiliar or risky.

Leading governments design around this reality, not against it. They treat behavioural intelligence as a core input to channel strategy, fraud controls, operational design, and payment method selection (choice). When behaviour and system design align, friction falls, cost falls, and trust rises.

Efficiency is not only an operational problem. It’s also a design and governance problem—especially when payment systems don’t reflect how citizens actually behave, or when end‑to‑end ownership is unclear.

If governments want to reduce cost, reduce fraud, and improve trust, they should stop designing payment systems around internal assumptions and start designing them around real human behaviour—supported by clear end‑to‑end accountability. When behaviour and system design align, efficiency follows. When they don’t, the system pays for the friction—every day.

👍

Great Article